EMAIL NEWSLETTER

MARCH 2014

Welcome

again to the McLean

and Co. Newsletter

in which we discuss current taxation and business matters. We trust

you find it informative.

We

are happy to accept new clients. We would be happy to assist colleagues

and acquaintances as new clients.

INDEX

-

Business Name Change

-

Office Closure

-

Year End

-

Income Tax Payments Due

-

New Minimum Wage Rates Take Effect from 1 April

2014

-

ACC Levy Changes from 1 April 2014

-

Easter and ANZAC Day Trading Hours

BUSINESS

NAME CHANGE

We're changing our business

name to TotalAccounting from 1 April, 2014. Apologies that you will

have to put up with old stock and name stationery for a little while, as our

professional body is combining with the Australian equivalent, and there

will be a new logo, so we are awaiting this before stationery reprinting,

and there are other stocks around which will eventually be

used

up. Also our website is in the process of being revamped and will be

still under McLean and Co. for a while. Eventually all will fall into

place.

OFFICE

CLOSURE

The Office is closed from

Wednesday 2/4/2014 until Friday 18/4/2014. The writer is off to the

South Island to ride the Central Otago Rail Trail and walk the Queen

Charlotte Sound Track. If you would like contact on return, leave a

message on the office telephone or by email.

YEAR

END

Year End for most taxpayers

is 31 March, 2014. Your "Business Documentation Required

for Preparation of Financial Statements" is in the Post.

The system we work to is list and see clients in order of when they call to

advise that they are ready. The list can mount up, so the earlier you

would like you work done the earlier you ring. We generally can't see

any clients until late May, as we have to wait for Tax Returns and Summary

of Earnnings for Wages for clients, and these aren't sent by IRD until that

date.

INCOME

TAX PAYMENTS DUE

Many clients have Terminal Tax to pay on or by 7 April, 2014 and

Provisional Tax to pay 7 May, 2014- you would have been advised if you have

to . Paying your bill on or before due dates l means you avoid any penalties

and interest. If you do miss the due date, it's never too late to pay

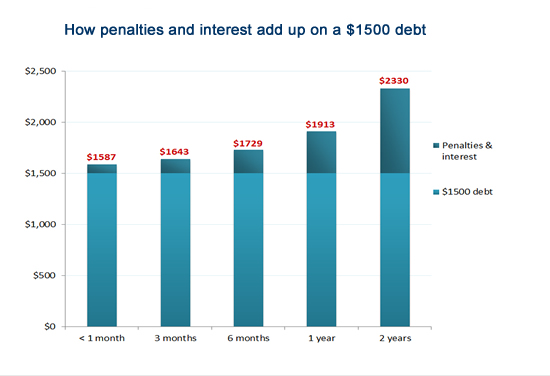

and stop more penalties and interest adding up.

This graph shows how quickly penalties and interest can add up on a

$1500 bill:

There are a range of options available for paying amounts due.

- You can pay in full.

- You can make an

instalment arrangement where you repay an agreed amount over time.

- IRD can write off an agreed amount if we determine that full

payment would cause you serious hardship.

- A combination of an instalment arrangement and a serious hardship

write-off.

If you are unable to pay the full amount due on time, you should

contact IRD as soon as possible. You do not have to wait until the due date

for payment has passed. You can phone IRD on 0800 227 771 or, if you are in

business or have a student loan, on 0800 377 771.

NEW

MINIMUM WAGE RATES TAKE EFFECT FROM 1 APRIL 2014

The new adult minimum wage rates

(before tax) that apply to employees aged 16 or over will be:

$14.25 per hour, which is

$114.00 for an 8-hour day,

$570.00 for a 40-hour week.

The Starting-out wage rates

and the training minimum wage rates (before tax) will increase

to:

$11.40 an hour, which is

$91.20 for an 8-hour day or

$456.00 for a 40-hour week.

The Starting-out wage

applies to:

- 16-

and 17-year-olds in their first six months of work with a

new employer (or until they are training or supervising

others)

- 18-

and 19-year-olds who have been paid a benefit for six months

or longer, and who have not completed six months of

continuous work with any employer since starting on benefit

(or until they are training or supervising others)

- 16-

to 19-year-old workers in a recognised industry training

course involving at least 40 credits a year.

The training minimum wage applies

to employees aged 20 years or over who are doing recognised

industry training involving at least 60 credits a year as part

of their employment agreement, in order to become qualified.

ACC

LEVY CHANGES FROM 1 APRIL 2014

ACC recently unveiled important changes to the ACC scheme effective from 1

April 2014.

These changes include a decrease in the ACC levy rates paid by all

self-employed people and businesses and an increase in the experience rating

loading from 50% to 75%.

Levy Rates

Levy rate decreases will reduce the cost of ACC cover for both

self-employed people and employers. These changes include:

- 17% decrease in the average Work levy

- 15% decrease on the Earners’ levy.

2014/15 Levy Rates at a Glance

| Who Pays and

How they Pay |

Current 2013/14 |

2014/15 Levy

Rates |

Percentage

Change |

|

Work Account

Levy

Cover for work injuries paid by self-employed people* and employers

(invoiced directly by ACC)

|

$1.15 |

$0.95^ |

-17% |

|

Earners’ Account

Levy

Cover for non-work injuries paid by employees (through PAYE) and by

self-employed people

|

$1.48 |

$1.26 |

-15% |

|

Motor Vehicle Account

Levy

Cover for motor vehicle injuries paid by motorists (through licensing

fees & petrol levy)

|

$330.68 |

$330.68^ |

No change |

Experience Rating Loading

Coinciding with the upcoming levy changes, experience rating loading will

increase for some businesses from April 1 2014. ACC are adjusting the loadings on

experience rating to more accurately reflect costs that businesses with higher

claims rates drive to the scheme.

Experience rating takes into account a business’s claims history when

setting its levies. Under experience rating, employers who have

lower-than-average injury rates, with better-than-average rehabilitation or

return to work rates, may receive a discount on their work levy. Those with

worse-than-average claims experience may receive a loading on their levy.

The experience rating discount will stay at 50% – however, the

calculation for businesses that have a worse-than-average claims experience

rating could increase from 50% up to 75%.

This increase is not only fairer for businesses whose safety performance is

average-to-excellent but should create an incentive for businesses with

worse-than-average performance to develop good health and safety practices.

EASTER

AND ANZAC DAY TRADING HOURS

With the Easter holiday period and ANZAC day fast approaching, now’s a

great time to take a look at your trading hours and your responsibilities for

paying staff.

All shops must be closed on Good Friday and Easter Sunday and any shops

that don’t comply are at risk of prosecution. The same applies on ANZAC day

before 1.00pm.

Some exemptions apply to ensure certain types of

essential services and shops remain open – such as restaurants, dairies and

service stations. You can find

out if your business is exempt by visiting MBIE online.

Employees who normally work on these days are entitled to a paid day off.

If your employees are required to work, they’re entitled to time and a half

for the hours worked on those days, and an alternative holiday if the day is

otherwise a working day for the employee.

Easter Sunday is not a public holiday – so there are no entitlements to a

paid day off or time and a half for hours worked on this day.

Easter and ANZAC day holidays for 2014:

- Good Friday Friday 18

April

- Easter Monday Monday 21

April

- ANZAC Day Friday 25

April

If you’re unsure about employee entitlements or

whether you’re able to open on these days, get in touch with MBIE's Contact

Centre before the Easter period.

The information provided in this email newsletter is for

informational purposes only. McLean and Co. accept no

responsibility for the opinions and information expressed in the

information provided and it is provided "as is" without

warranty of any kind. The user assumes the entire risk

as to the accuracy and use of this document. Readers are

asked to seek professional advice pertaining to their own

circumstances. The McLean and Co. email newsletter may

be copied and distributed subject to the following conditions:

If we

can assist further, please email McLean and Co as follows:

CONTACT

McLEAN AND CO. BY EMAIL BY CLICKING ON THIS LINK

BACK TO HOME PAGE