INCREASE IN THE MINIMUM WAGE

The minimum wage will increase from the current $13 per hour to $13.50 an hour, the Government had

announced. The training and new entrant minimum wage will increase from $10.40 to

$10.80.

This comes into effect on April 1, 2012.

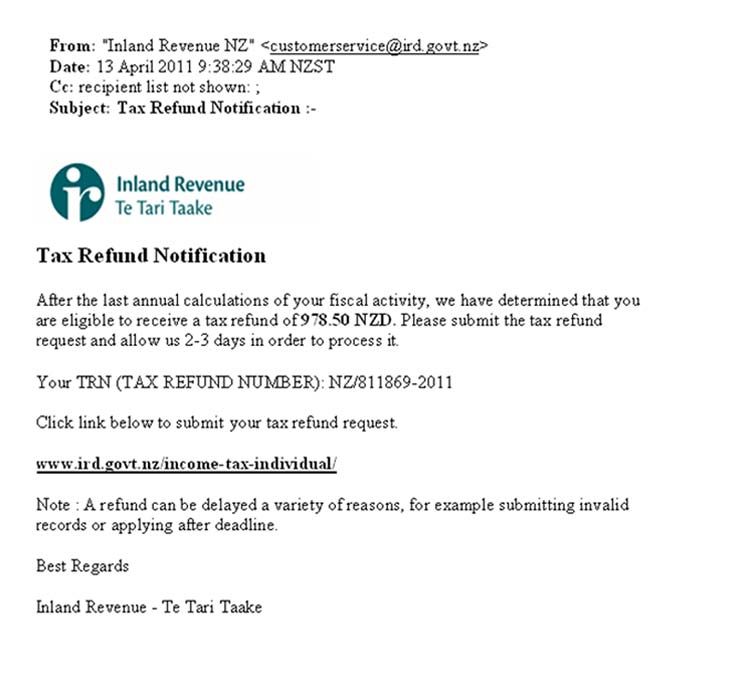

WARNING ABOUT SCAM EMAILS

PURPORTING TO BE FROM INLAND REVENUE DEPARTMENT

Be ultra careful about giving out your IRD number and any other

personal details to email callers.

Emails can circulate which attempt to trick recipients into divulging

personal information. These emails are known as phishing emails. For

example, an email may claim to come from Inland Revenue or a Tax Refund

Agency asking you to click on a link that takes you to a fake website.

Do not click a link, or reply to an email, fitting this description.

Inland Revenue will not send you a hyperlink in an email. Delete the email

from your Inbox and Trash folders.

The following is an example of a scam email which McLean and Co, and

we are aware a number of clients have received also:

THE PROFIT AND LOSS STATEMENT

The Profit and Loss statement (or statement

of financial performance) provides a picture of your business trading

performance over the last accounting period - usually a year, and

generally from April 1st of one year to March 31st

of the year after. It records sales, costs and expenses, profits (or losses), and any

tax payments for the period. This is the document that Inland Revenue

uses to determine what tax you owe, so it is important that you

understand how it works.

The Profit and Loss statement usually follows this relatively easy

format:

Turnover

(or sales).

Less: cost of sales (your 'direct' costs,

such as raw materials).

Equals gross

profit (turnover less cost of sales).

Less: fixed or 'indirect' costs (also

called business overheads) such as rent, rates and salaries. This will

include depreciation on fixed assets.

Equals

operating profit or net profit before tax.

Less: tax payable.

Equals net

profit after taxation

The Profit and Loss statement is usually straightforward and

relatively easy for non-financial managers to understand., but you might

need to ask questions about some elements of the statement to understand all

the information in it.

Some things aren't included. For example, the principal repayment of

a loan is not included in the Profit and Loss statement, because it does

not count as an expense, in the same way that injecting additional

capital doesn't count as sales. But the interest you pay on a loan is an

expense that you would include.

As a business owner, you'll want to claim as many legitimate expenses

as possible to keep the tax bill down; however, it is important not to

rush out and buy things you don't really need just to reduce your tax

bill. You'd be better off making a higher profit and paying a little

extra tax, than a lower profit and spending your hard earned cash on

things you don't need.

What can you do with the profit and loss statement?

The best use of your profit and loss statement is to look at your

profit margins, and to see if any expenses have increased dramatically

since last year.

Gross profit: Your gross profit

margin is your gross profit as a percentage of turnover. For example, if

your turnover is $2mn with a cost of sales of $600,000, you have a gross

profit of $1,400,000 and a gross profit margin of 70% (1,400,000 ÷ 2,000,000

x 100). So every $100 of sales generates $70 that goes towards paying

for expenses (and towards your profit). If this percentage starts to

slip over time, it is an indication that you need to take action. Find

out why. Some reasons include:

- Rising inventory costs

- Offering discounts

- Theft by customers or staff

- Selling products that have lower margins.

Net profit: Your net profit margin

compares your net profit (gross profit less fixed or indirect costs) to

turnover. For example, for a business with a turnover of $2m and an

operating profit of $300,000, the operating profit margin would be 15%

($300,000 ÷ $2,000,000 x 100). Again, if this falls, it means you

are paying proportionately more in expenses (rent, power, salaries,

etc.) than you should be.

This is particularly useful in pointing to

problems when you don't expect them, for example when your net profit

is going up. Using the above example, if your sales increased to $3mn

and net profit was up at $400,000, this looks good. But while your

profit is up, your net profit percentage has fallen ($400,000 ÷

$3,000,000 x 100) to 13.3% from 15%.

DRIVERS OF PROFIT AND CASHFLOW

Profit and Cashflow is the lifeblood of a business and significant

factors in the success of any business. The following are significant

factors related to these:

Revenue Growth Percentage

Allowance for the fact that invariably you have to pay for the stock/

labour to produce the sale, before you make the sale. You have to be

in a position to fund the sale in these circumstances.

Price Change Percentage

This is a consequence of any price adjustments, be they increase ,

decrease or discount. Margins should be monitored to see when it is time to

increase prices. Many business think they can't increase prices because they

lose customers, but most people understand that prices go up- wages and fuel

go up constantly. When your suppliers prices go up use this

opportunity to increase yours. If you dont increase prices regularly,

gross profit will reduce and your overall profit and cashflow will be

significantly affected

Cost of Goods Percentage

This relates to the comparison of your sales price and the direct

costs of the stock/ materials purchased to achieve those sales. The setting

of the value of your sales prices by yourself, your reaction to

increased, decreased prices charges by your Suppliers can increase or

decrease the Cost of Goods Percentage, which is an impostant factor in

Profit or Cashflow. In your Financial Statements, the Sales less the

Cost of Sales is your Gross Profit. If your Gross Profit is less than

your Overheads you will make a Loss. Therefore it

is important to achieve a Cost of Goods Percentage which is to your

financial favour.

Overheads Percentage

Overheads occur all the time e.g. wages, rent, power, telephone.

Your overheads will continue even if you are not achieving sales at the

time. It is therefore important to contol Overheads. A good way to do

this is to prepare a budget for the year, and regularly compare this budget

against actual. You should also be flexible and change your budgets if

your business circumstances markedly change during the year.

Accounts Receivable Days

This is the number on days, on average, that customers are taking to

pay. Regular follow up is one way of decreasing Accounts Receivable

days. It should be remembered that your customers supply all the cash

to run your business

Accounts Payable Days

This is the number on days, on average, taken to pay suppliers. It is

common to see this number at less than the Accounts Receivable days

number. Such actions can result in a cash squeeze. so Accounts

Receivable days are important to avoid this.

Inventory and Work in Progress Days

Inventory days is the number of days, on average, stock sits in store

waiting to be sold. Work in Progress days is the number of days jobs are in

progress prior to invoicing. You need to have stock ready to sell when

customers are ready to buy, but not too long , as this will suck up working

capital. With reference to Work in Progress (which would involve you paying

out wages, buying stock etc. accordingly for same) , the longer it takes to

complete jobs and invoice, the more working capital is needed , Speeding up

job management and reducing Work in Progress days will have a positive

impact on cash. Interim/ Progress charges may be appropriate and necessary,

so that your business cash flow is not affected, if there is a reasonable

lengthy period before completion of a job.

The information provided in this email newsletter is for

informational purposes only. McLean and Co. accept no

responsibility for the opinions and information expressed in the

information provided and it is provided "as is" without

warranty of any kind. The user assumes the entire risk

as to the accuracy and use of this document. Readers are

asked to seek professional advice pertaining to their own

circumstances. The McLean and Co. email newsletter may

be copied and distributed subject to the following conditions:

If we

can assist further, please email McLean and Co as follows:

CONTACT

McLEAN AND CO. BY EMAIL BY CLICKING ON THIS LINK

BACK TO HOME PAGE